The Kitchen Multiverse

Dark kitchens, cloud kitchens, ghost kitchens, virtual kitchens…. These terms have been increasingly permeating consumers’ vocabulary, industry research papers and articles in recent times. But does anyone really know the difference between each of them?

By broad definition, ghost kitchens are a new business model in which virtual or existing restaurants use equipped kitchen spaces with no dine-in facilities and connect directly with delivery platforms to enhance their online food delivery capabilities. Their main advantage over traditional restaurants is the significantly lower upfront investments needed to open a new location; reflected on lower costs in Real Estate and personnel (ie. no waiters, hosts or bartenders), lower (and almost organic) customer acquisition costs, and larger economies of scale and scope.

These new business models surged from the rising demand of food delivery platforms, such as Uber Eats, GrubHub, DoorDash, Deliveroo, Swiggy, Foodpanda and Rappi, who have altogether raised more than USD$20bn of VC investment in the past years. The non-stopping growth in food delivery platforms and the current COVID-19 pandemic have driven shifts on customer behavior; boosting the importance of off-premise dining and forcing brick-and-mortar restaurants to streamline and digitalize their operations to offer a quality service for their new virtual inbound customers.

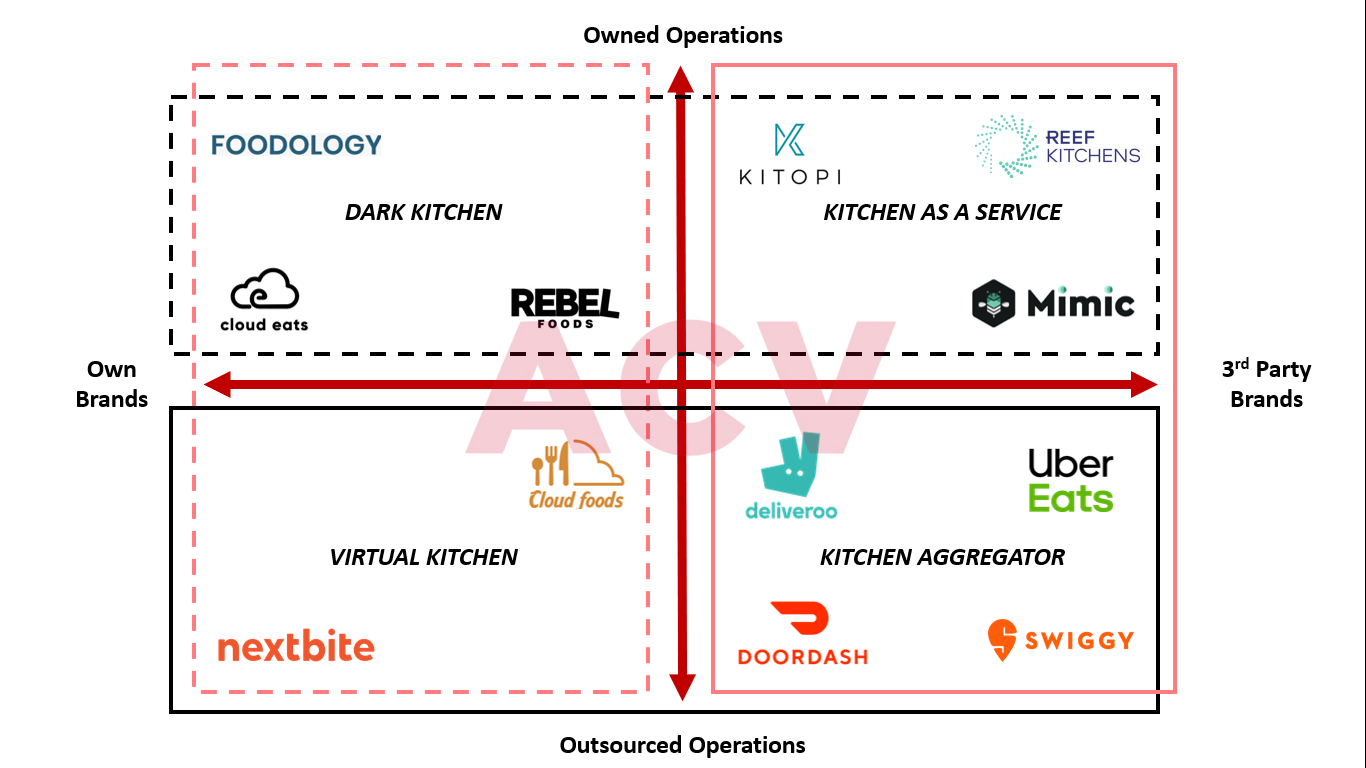

After a series of conversations with multiple startups and investors, we have designed the following Kitchen Multiverse Matrix which describes these new business models based on the level of control in operations and brand management.

The Kitchen Multiverse Matrix

- Dark Kitchen is the traditional ghost kitchen model, in which existing or new restaurants lease ready-to-use kitchen spaces or a facility they adapt as a kitchen, bring-in their own equipment and labor in order to cook their own menus under their own brands. The source of power comes from a smooth operation and brand positioning within target segments. Typically, dark kitchens define their food verticals (ie. chicken, beef, fish, vegan, paleo, Asian, Italian, Mexican, etc.) and the brands’ segmentation (based on socio-economical analytics). Their revenue source is the income generated by food sale, as if they were a traditional restaurant. Some examples within the category are CloudEats in the Phillipines and Foodology in Colombia.

2. Kitchen-as-a-Service companies, like Kitopi in Dubai and Mimic in Brazil, manage their own kitchen operations and prepare the food on behalf of a third-party restaurant under a franchise model, paying them a royalty fee. The main purpose is to make restaurant lives easier and solve operations and last-mile pain points. The key strength of this player is the operational capability and flawless execution supported by a degree of automatization through the utilization of technology.

3. Virtual Kitchen is a counterparty of the KaaS model. It leverages from data analytics to define respective target segments and create brands and menus. They are not involved at all in kitchen operations, but instead focus their efforts into building brand recognition and customer loyalty. Virtual kitchens, such as Nextbite in the US and Cloud Foods in Brazil, capture a percentage of the total product revenues as if it were a royalty payment.

4. Kitchen-Aggregators are typically delivery platforms that procure increasing the number of food brands hosted in their apps. Technology is the greatest differentiator, creating large communities of customers and offering delivery capabilities to restaurants. They also leverage the data gathered from their delivery activities to boost the performance of their restaurant partners. Typically, companies such as Uber Eats (US), Deliveroo (UK), Swiggy (India), and Rappi (Colombia) get a commission on the delivery and a share of the profits when they partner with the dark kitchens.

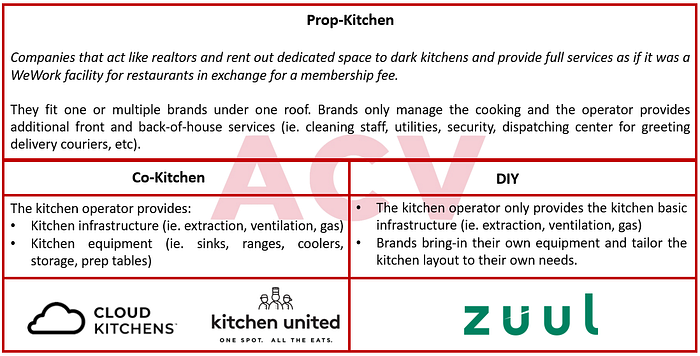

5. Dark kitchens and Kitchen-as-a-Service companies have a necessity for Real Estate. A fifth model is the Property-Kitchen, which is based on Real Estate capabilities. Users could either consider the ready-to-use kitchen spaces (co-kitchen model) or the do-it-yourself approach (traditional space lease). Some companies that operate in this space are Cloud Kitchens (funded by Uber co-founder, Travis Kalanick) and Kitchen United (with Google Ventures as investor), both based in the US. They rent out the spaces to dark kitchens or kitchen-as-a-service companies and provide full services as if they were a WeWork facility for restaurants in exchange for a membership fee. Some of them have a proprietary delivery platform, from which they get a take-rate on the food order value.

Additional considerations

Additional considerations (though not limited) for new incumbents wanting a piece of the cake are:

· Not a one-size-fits-all type of model. Many ghost kitchen startups operate in multiple quadrants within the Kitchen Multiverse Matrix.

· Tech stack development is a great source of competitive advantage (ie. dispatching efficiency, centralized order management system, multi-cuisine ordering, etc.)

· Use of complementary channels is allowed, such as take-out, store front, catering or limited dine-in solutions.

· Level of reliance in delivery platforms (proprietary vs 3rd party), vertical integration of the supply chain and data leverage can create endless business opportunities.

In summary, these new business models are on the rise and it is important to understand them under the Kitchen Multiverse Matrix’s elements: operations, brands and RE; where companies might compete in one or multiple categories. It is also important to note that new business models will continue to surge, some players will disappear and some others will survive; but while the future is still uncertain, just grab your phone and order a burger! As Niccolo Machiavelli said: “there is nothing more difficult to take in hand, more perilous to conduct, or more uncertain in its success, than to take the lead in the introduction of a new order of things”.

Written by:

Hector Shibata. Director of Investments & Portfolio at ACV a global Corporate Venture Capital (CVC) fund and Adjunct Professor for Entrepreneurial Finance.

Gonzalo Soriano. Investment analyst at ACV.

ACV is an international Corporate Venture Capital (CVC) fund investing globally in Startups & VC funds.

Stay updated about Venture Capital, innovation, entrepreneurship and more! Sign up for AC Venture’s monthly Newsletter.

Follow us on LinkedIn: ACV_VC

Follow us on Twitter: acv_vc

Follow us on Spotify: https://open.spotify.com/show/5K0i5z43ZM3PLiDs9Sa8Px?si=FIAJuB_CSN-3MWKC3Qn7Qw